Most people think real estate investors get rich from rent checks.

They do. But the tax code is built for business owners and entrepreneurs. Depreciation is one of the biggest reasons wealthy people use real estate. Not because they cheat. Because they understand a rule most W-2 earners never learn.

If you own rental property and you're not using depreciation on purpose, you're probably overpaying.

What goes wrong when you skip this

Not knowing your numbers is like driving somewhere new without GPS. You'll get somewhere. You just won't know if it's where you wanted to go.

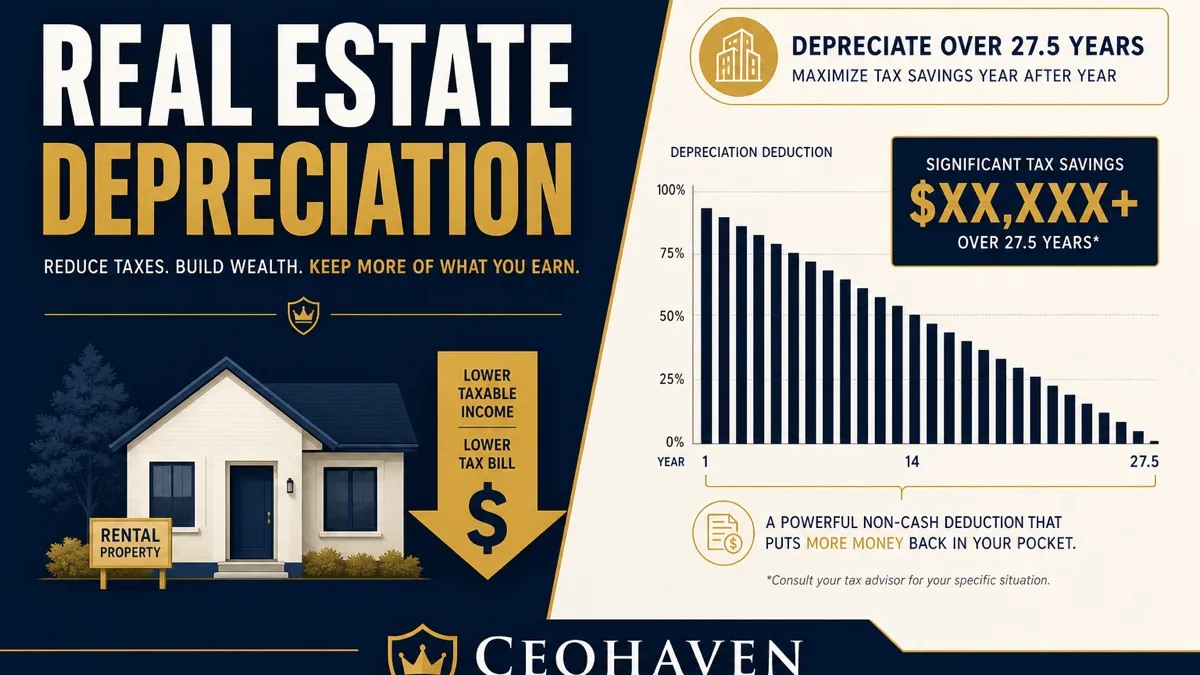

A lot of rental owners track rent and mortgage payments. They forget the building itself is a tax asset. The IRS lets you write off wear and tear on the structure over time, even when the property is going up in value.

That mismatch is the whole game.

Picture this: You buy a rental for $400,000. Land is worth $80,000. The building is $320,000. Over 27.5 years, you can deduct about $11,600 a year in depreciation on the building alone. That's real money off your taxable income every year, while tenants pay down your loan and the property can still appreciate.

Skip that deduction and you're paying tax on income the tax code already said you could offset.

The triple benefit (why investors stay in real estate)

With real estate you get three things at once:

- Cash flow from rent

- Appreciation when the property goes up in value

- Tax benefits from depreciation and other write-offs

This is what billionaires and millionaires use to keep more of what they earn. Not a promise you'll pay zero tax. A strategy that exists in the code on purpose. Regular people are meant to use the same tools. Most just never get taught how.

Depreciation is the tax benefit most new investors hear about last. It should be one of the first things you plan around.

Depreciation in plain English

Depreciation means spreading the cost of a business asset over its useful life.

For rental property, you're not writing off the whole purchase price in year one (with some exceptions we'll touch on). You're taking a piece of the building's value each year as a deduction.

Important details most people miss:

- Land doesn't depreciate. Only the building and certain improvements count.

- Residential rentals (most houses, duplexes, apartments rented long-term) use a 27.5-year schedule per IRS Publication 946.

- Commercial property generally uses 39 years.

- You need a cost basis split: purchase price minus land value, plus certain closing costs and capital improvements.

Your CPA or advisor should document how you split land vs. building. "I guessed 20%" doesn't hold up well if anyone asks.

How the math actually works

Say you buy a long-term rental for $550,000.

- Land value: $110,000 (not depreciable)

- Building: $440,000 (depreciable)

- Annual depreciation: $440,000 ÷ 27.5 = $16,000 per year

You also deduct mortgage interest, property taxes, insurance, repairs, property management, and travel for the business. Add it up and your taxable rental income can be a lot lower than the cash sitting in your bank account.

Example: Gross rent $42,000. Expenses (not counting depreciation) $18,000. Cash flow before depreciation looks like $24,000.

Then depreciation hits: $16,000.

Taxable rental income on paper: $8,000, even though you collected more cash than that.

That's not a loophole in the sketchy sense. It's how rental income and expenses work on Schedule E.

Side-by-side: what depreciation changes on your return

| Factor | Without planning | With depreciation tracked |

|---|---|---|

| Taxable rental income | Often close to cash collected | Usually lower on paper |

| Cash in your pocket | Same | Same |

| Audit risk | Higher if you guess | Lower with documented basis |

| Long-term planning | Reactive | You see the number before year-end |

The table doesn't replace a pro running your actual return. Your mortgage, expenses, and other income all change the outcome.

The catch: passive loss rules

Here's where people get surprised.

Depreciation can create a paper loss (expenses plus depreciation exceed rent). That loss doesn't always wipe out your W-2 income automatically.

Rental real estate is usually a passive activity. Passive losses generally only offset passive income unless you qualify for an exception.

Common paths investors talk about:

- Material participation in your rentals (real work, real hours, real records)

- Real Estate Professional Status (REPS) for people who spend enough time in real estate activities

- The short-term rental rules for certain Airbnb-style properties (different rules, strict tests)

If you're a high-earning W-2 employee with one passive rental and no plan, a paper loss might just sit on the shelf as a suspended loss until you have passive income or sell the property.

That's not a reason to skip depreciation. You still want the deduction on the books. But you need to know whether it helps you this year or stacks for later.

This is advisor territory, not a blog guess. Run your hours, your activity, and your income with someone who does this for investors.

Depreciation recapture (don't ignore the exit)

Depreciation lowers your tax bill while you own the property. The IRS remembers.

When you sell, you may owe depreciation recapture taxed up to 25% on the depreciation you took (or could have taken). Publication 544 covers sales of business property.

Planning the hold period, a 1031 exchange, or your long-term exit matters. Depreciation is a tool for building wealth, not a free pass that never gets settled.

Read this before you go advanced: the $400K line

If you're under $400,000 a year total, don't blow up your life chasing every real estate tax move. Get your first property structured right, track depreciation from day one, and focus on making more.

This article is for investors who already own rentals, or who are serious about real estate as a wealth tool and want to understand why depreciation shows up in every serious tax conversation.

Past $400K, taxes become one of your biggest expenses. That's when cost segregation, entity structure, and participation rules stop being "someday" topics and start being money on the table.

What I set up with real estate clients

Not theory. The checklist.

1. Cost basis worksheet from day one

Purchase price, land allocation, closing costs that get added to basis, and every capital improvement (new roof, HVAC, major remodel). Depreciation starts from the right number. Fix it later and you're guessing.

2. Separate schedules for the building vs. improvements

A new roof might depreciate over 27.5 years on a residential rental. Some items qualify for faster write-offs. Your advisor decides what goes where. You decide to keep receipts.

3. Monthly bookkeeping tied to the property

Rent in, expenses out, loan principal vs. interest split. A tax plan is like a personal trainer giving you a workout plan. Someone still has to do the reps. If the books are messy, depreciation won't save you from a bad year-end scramble.

4. A participation log if you're chasing active losses

Google Calendar, a spreadsheet, whatever you use. If you're arguing you're actively involved in your rentals, prove the hours. The IRS doesn't take your word for it.

5. An annual review before December 31

Income up? New property? Refi? That changes the plan. Founders and investors who only think about taxes in March are always reacting. The savings are in the moves you make before the year closes.

Mark Kohler's The Tax and Legal Playbook puts it simply: the tax and legal side isn't separate from the asset. It's part of how you buy and hold.

Who this is for

Active or aspiring real estate investors who want to understand depreciation, not just hear the word at a seminar.

If you're brand new and still saving for your first down payment, keep learning. But don't pay for advanced strategy you can't use yet. Make more, get your first deal clean, and build from there.

No shame. Just honest.

The short version

- Depreciation lets you deduct the building's cost over time, even while the property may gain value.

- Land doesn't depreciate. Split land vs. building and document it.

- Residential rentals: 27.5-year schedule. Commercial: 39 years.

- Paper losses from depreciation don't always offset W-2 income. Know the passive activity rules.

- Depreciation recapture can hit when you sell. Plan the exit, not just the purchase.

- Under $400K, get basics right. Above $400K, advanced real estate tax strategy starts to pay for itself.

- Track basis, improvements, and hours from day one. Clean records beat clever tricks.

FAQs

What is depreciation for rental property?

It's an annual tax deduction that spreads the cost of the building (not land) over its useful life. For most residential rentals, that's 27.5 years. It lowers taxable rental income even when you're collecting rent and the property may be appreciating.

How do you calculate depreciation on a rental property?

Start with depreciable basis: purchase price minus land value, plus certain closing costs and capital improvements. Divide by 27.5 for residential long-term rentals. Example: $440,000 building basis ÷ 27.5 = about $16,000 per year.

Can depreciation reduce my W-2 taxes?

Sometimes, but not automatically. Rental losses are often passive and may only offset passive income unless you qualify through material participation, Real Estate Professional Status, or certain short-term rental rules. Run your specific situation with a tax advisor.

Do I have to depreciate my rental property?

The IRS generally expects you to take allowable depreciation. If you skip it, you may still owe recapture on the amount you should have taken when you sell. Don't ignore it.

What happens to depreciation when I sell?

You may owe depreciation recapture on prior deductions, taxed up to 25%. Your total gain on sale can also trigger capital gains tax. A 1031 exchange may defer some taxes if you meet the rules. Plan before you list.

Is cost segregation the same as regular depreciation?

Cost segregation is a study that breaks a property into parts that can depreciate faster (five, seven, or fifteen years in some cases). Regular depreciation is the default straight-line method over 27.5 or 39 years. Cost segregation can front-load deductions but adds cost and complexity. It's usually for larger or more active portfolios.

References

- IRS — Publication 527, Residential Rental Property

- IRS — Publication 946, How to Depreciate Property

- IRS — Topic 414, Rental Income and Expenses

- IRS — Publication 925, Passive Activity and At-Risk Rules

- IRS — Publication 544, Sales and Other Dispositions of Assets

What to do next

Own rentals but never mapped your cost basis? Taking depreciation without knowing if those paper losses actually help your W-2 situation? That's fixable, but you need a plan built on your properties, not a generic article.

At CEOHAVEN, we help entrepreneurs and real estate investors with tax planning, tax preparation, and bookkeeping. You should actually know your numbers, not just collect rent and hope April goes fine.

Book a call. We'll look at your properties, your participation, and what depreciation should be doing for you this year.

It's not about how much you make. It's about how much you keep.